Comunicati Stampa - Italia - BFF Banking Group

Press Releases

03 Aug 2023 - 11:30

| Relevant information

BFF Banking Group announces record 1H23 adjusted consolidated net profit and EUR 0.438 of dividend per share

- 1H23 Reported Profit at €76.1m, +34% YoY, Adjusted Net Profit at €81.9m, +20% YoY, best 1H ever.

- Strong growth in Loan Portfolio, at €5.3bn, +16% YoY, a new historical 1H high.

- Robust Balance Sheet with stable and diversified funding and no recourse to ECB lending facilities. Loan/Deposit ratio at 71%, with net positive inflow of retail deposits in 1H23.

- Improved Leverage Ratio, with reduction in Total Assets and increase in loan book YoY.

- Strong asset quality with 0.1% Net NPLs/Loans ratio excluding Italian municipalities in conservatorship.

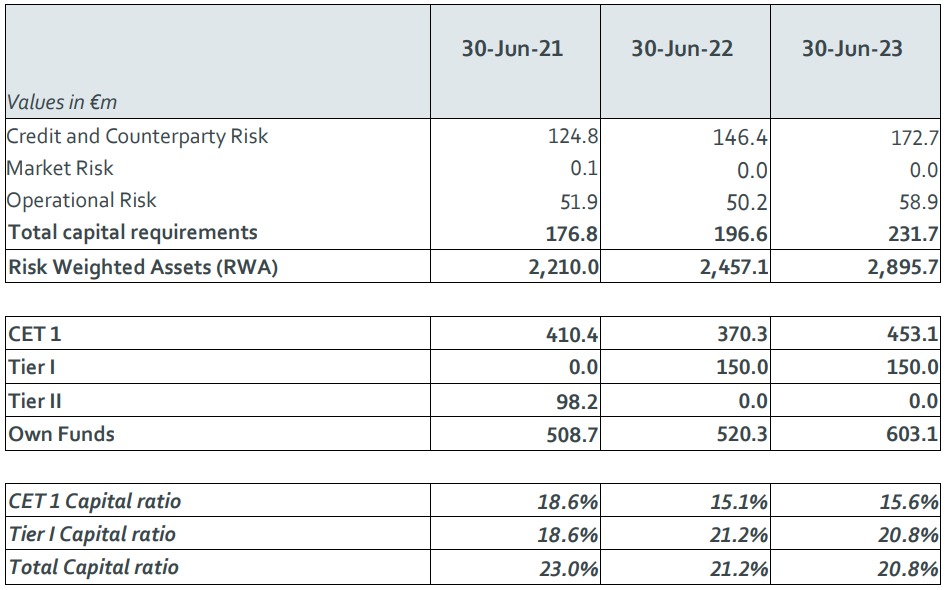

- Very solid capital position: CET1 ratio at 15.6% and TCR at 20.8%. €106m of excess capital vs. 12% CET1 ratio target.

- Distribution of a dividend equal to €81.9m (€0.438 p.s.), +18% YoY, with payment day on 13th September 2023, to be paid following GSM of 7th September 2023.

- New 2028 strategy and 2026 medium-term targets presented on 29th June during Investor Day.

Milan, 3rd August 2023 – Today the Board of Directors of BFF Bank S.p.A. (“BFF” or the “Bank”) approved BFF’s first half 2023 consolidated financial accounts.

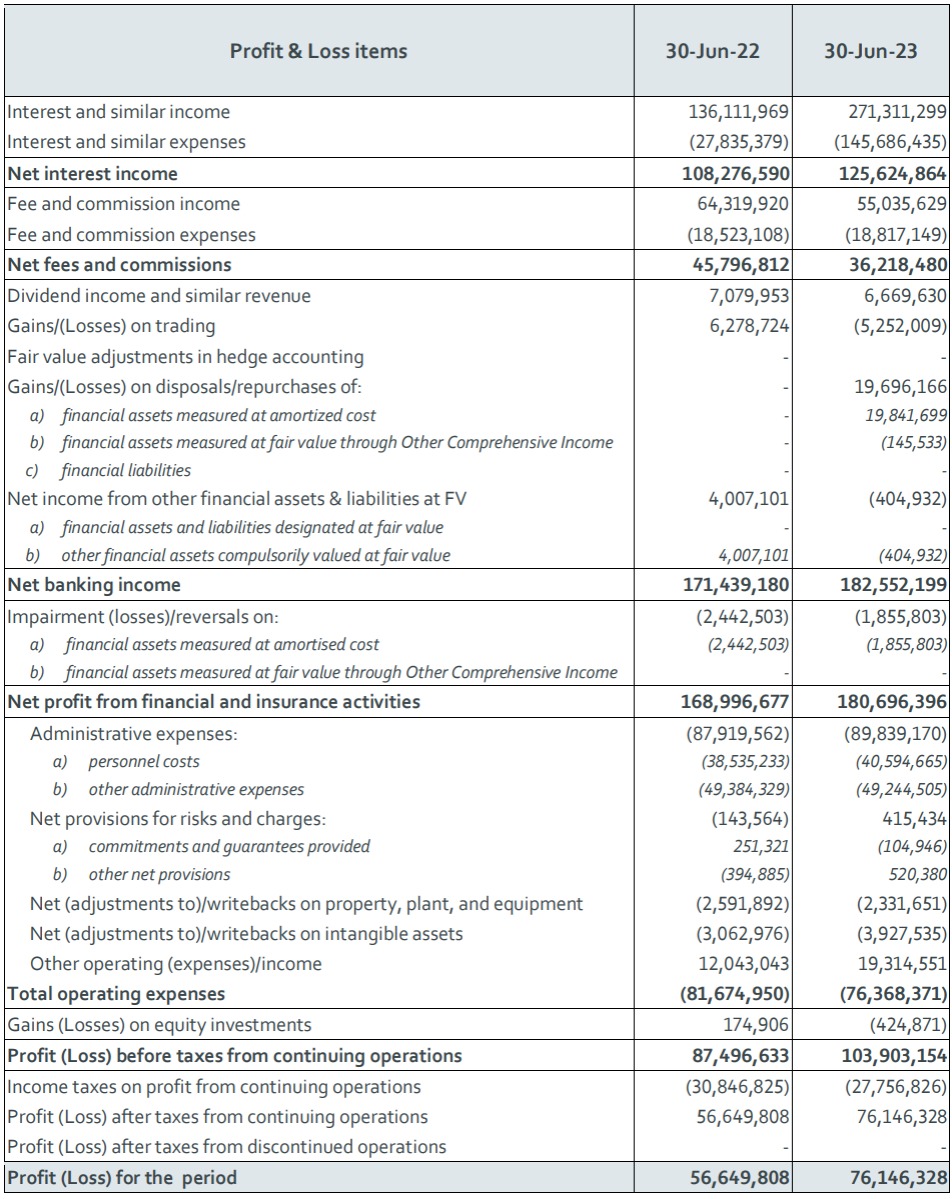

CONSOLIDATED PROFIT AND LOSS

1H23 Adjusted Total Revenues were €352.8m (+72% YoY), of which €186.1m coming from Factoring, Lending & Credit Management business unit, €29.2m from Payments, €12.4m from Securities Services and €125.1m from Other Revenues, of which €78.6m from the Government bond portfolio. 1H23 Cost of Funding was at €150.9m, with liabilities repricing faster than assets, and Adjusted Total Net Revenues were €201.9m (+11% YoY). Total Adjusted operating expenditures, including D&A, were €88.0m (€82.4m in 1H22), and Adjusted LLPs and provisions for risks and charges were €1.9m.

This resulted in an Adjusted Profit before taxes of €112.0m, and an Adjusted Net Profit of €81.9m, +20% YoY. 1H23 Reported Net Profit was €76.1m, +34% YoY (for details, see footnote n° 1).

With regard to the business units’ KPIs and adjusted Profit & Loss data, please refer to the “1H 2023 Results” presentation published in the Investors > Results > Financial results section of BFF Group’s website. Please note that the Corporate Center comprises all the revenues and costs not directly allocated to the three core business units (Factoring, Lending & Credit Management, Payments and Securities Services).

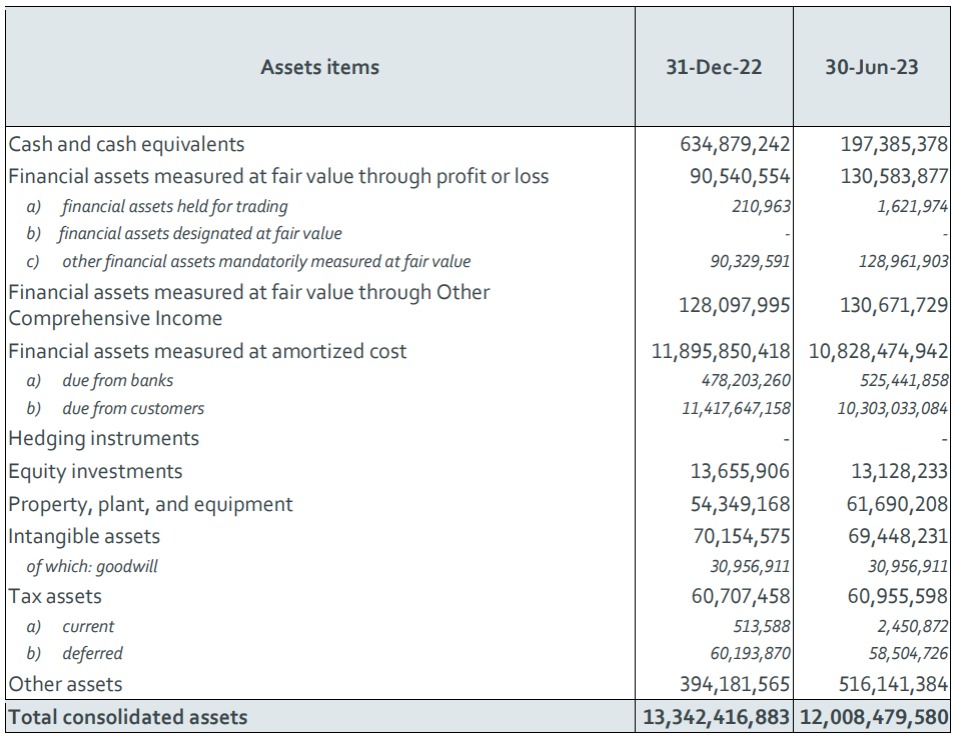

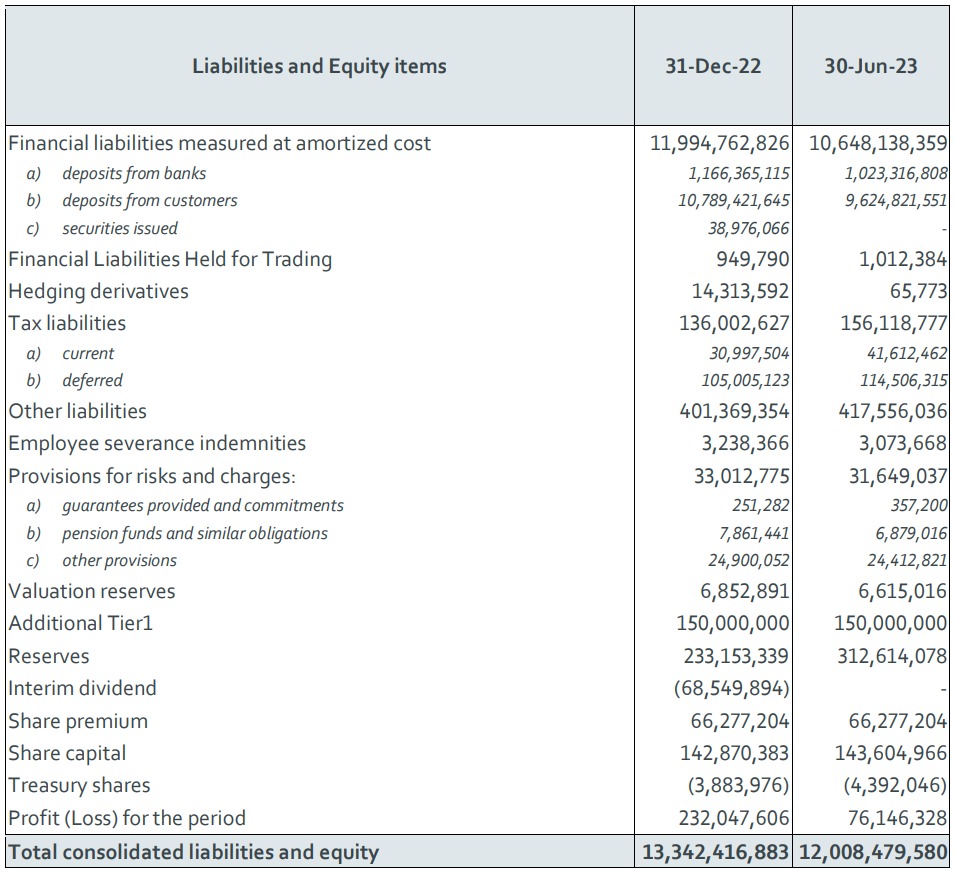

CONSOLIDATED BALANCE SHEET

As of 30th June 2023, the consolidated Balance Sheet amounted to €12.0bn down by €0.4bn (-4%) vs. the end of June 2022, despite the increase in Loan Book YoY.

The Loan Book was at €5,252m , at a new 1H historical high, up by €724m YoY (+16%), with strong performance of Greece up by 49% YoY and Portugal, up by 34% YoY.

At the end of June 2023, the Government bond portfolio was classified entirely as Held to Collect or “HTC”. The bond portfolio was equal to €5.2bn at the end 1H23, vs. €6.0bn at the end of June 2022, with a strong reduction of fixed bonds – 21% of the total portfolio in 1H23 vs. 47% in 1H22. The fixed bond portfolio residual average life was 47 months, with a yield of 0.70%; the floater bond residual portfolio average life was 68 months, with a spread +0.89% vs. 6-month Euribor and a running yield of 4.51% as of 30th June 2023. Cash and Cash Balances were €197m as of end of June 2023, down by €190m (-49%) YoY.

On the Liabilities side, the main changes vs. end of June 2022 are the following:

- deposits from Transaction Services were €5.6bn at the end of June 2023, down by €2.2bn YoY (€0.7bn YoY excluding Arca), primarily due to Arca’s exit;

- on-line retail deposits at end of June 2023 amounted to €1,744m vs. €307m at the end of June 2022, up by €1,437m (>100%) YoY, primarily raised in Spain and Poland;

- Passive Repos (refinancing operations related to Italian Government Portfolio) amounted to €3.2bn at the end of June 2023, vs. €2.9bn at end of June 2022, up by 10% YoY;

- BFF did not have any outstanding Senior unsecured bonds at the end of June 2023 (vs. €39m at end of June 2022), due to the repayment at maturity of the residual amount of €39m referred to the Bond issued in October 2019 with maturity May 23rd 2023.

Cost of funding in 1H23 was 2.75%, lower than the average market reference rates.

BFF does not have European Central Bank “ECB” funding to be refinanced (PELTRO, TLTRO, etc.).

The Group maintained a strong liquidity position, with Liquidity Coverage Ratio (LCR) at 312.3% as of 30th June 2023. At the same date, the Net Stable Funding Ratio (NSFR) was 159.1% and Leverage Ratio 5.0%, improved vs. 4.6% at YE22.

***

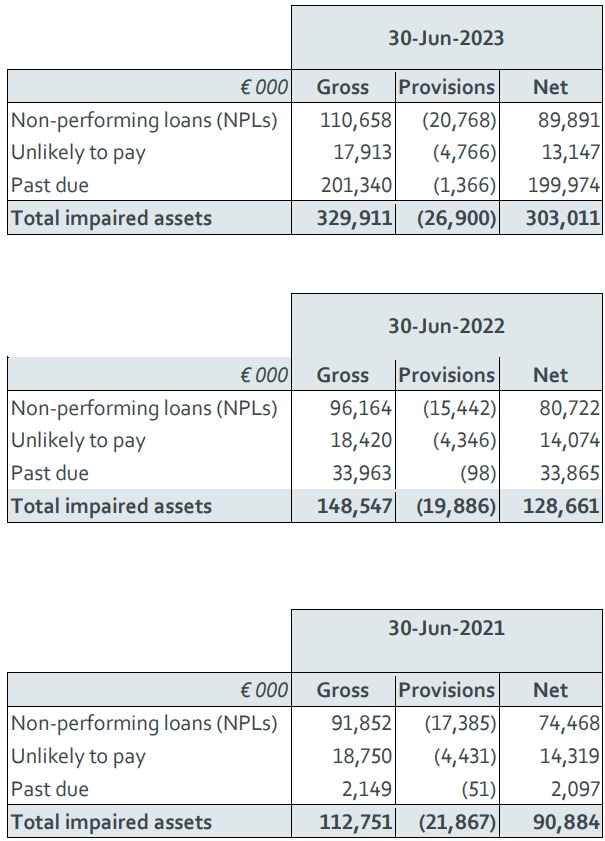

Asset quality

The Group continues to benefit from a very low exposure towards the private sector. Net non-performing loans (“NPLs”), excluding Italian Municipalities in conservatorship (“in dissesto”), were €6.6m, at 0.1% of net loans, with a 76% Coverage ratio, improved vs. YE22 and vs. 1H22 when it was 74% and 68%, respectively. Italian Municipalities in conservatorship are classified as NPLs by regulation, despite BFF is entitled to receive 100% of the principal and late payment interests at the end of the conservatorship process.

Negligible annualized Cost of Risk at 7.3 basis points at end of June 2023.

At the end of June 2023 net Past Due amounted to €200.0m, increased vs. €185.3m as of YE22 and vs. €33.9m as of end of June 2022. In September 2022 Bank of Italy issued more stringent interpretation criteria on the DoD (Guidelines on the application of the definition of default under Art. 178 of Regulation (EU) no. 575/2013), determining a step up in Past Due exposure, with no impact on the Group underlying credit risk: 91% of NPE exposure is towards Public Administration in 1H23.

Total Net impaired assets (non-performing, unlikely to pay, and past due) were €303.0m as of 30th June 2023, vs. €283.8m as of YE22, and €128.7m as of end of June 2022, primarily as a consequence of higher Past Due.

Capital ratios

The Group maintains a strong capital position with a Common Equity Tier 1 (“CET1”) ratio of 15.6% vs. a SREP of 9.0%. The Total Capital ratio (“TCR”) is at 20.8%, vs. a SREP of 12.5%. Both ratios exclude €81.9m of accrued dividends, which, if included, would bring CET1 ratio and TCR at 18.5% and 23.7% respectively. BFF has €106m of excess capital vs. 12% CET1 ratio target. The target capital ratio, as announced on 29-Jun-23 during BFF Capital Market Day , has been moved from 15% TCR to 12% of CET1 ratio , to align it with other banks main capital target. Distribution of dividends remains, as before, subject to the fulfillment of all the regulatory capital requirements, with dividend confirmed twice a year, in August and April, based on 1H and full year Adjusted Net Income.

Risk Weighted Assets (“RWAs”) calculation is based on the Basel Standard Model. As of end of June 2023 RWAs were €2.9bn, increased vs. €2.7bn at YE22 and vs. €2.5bn at end of June 2022 due to a higher Loan Portfolio YoY, with a density of 44%, vs. 42% at YE22 and 41% at end of June 2022.

***

Dividend per share of €0.438

Today, BFF Board of Directors resolved:

- to distribute an interim dividend before taxes based on the results as of 30th June 2023, equal to €0.291 per share, for a maximum total amount of €54,451,024.78, for each of BFF outstanding ordinary shares, net of the treasury shares held by the Bank at the record date;

- to convene the Shareholders' Meeting (the "Shareholders' Meeting"), in ordinary session on 7th September 2023, in a single call to approve the proposal to distribute part of the retained earnings reserve of BFF Bank S.p.A. as of 31st December 2022, equal to €0.147 per share, for a maximum total amount of €27,487,349.74, for each of BFF outstanding ordinary shares, net of treasury shares held by the Bank at the record date.

Following the approval of the Shareholders’ Meeting, BFF will distribute a total of €0.438 per share (for a maximum total amount of €81,938,374.52, the consolidated Adjusted Net Profit of the Group).

The payment, in agreement with Borsa Italiana S.p.A., pursuant to art. 2.6.2 of the Regulations of Markets organized and managed by Borsa Italiana S.p.A., as well as art. IA.2.1.2 of the related Instructions, will take place on Wednesday 13th September 2023, with ex-dividend date of coupons n° 8 and n° 9 on Monday 11th September 2023, and record date (i.e., date of entitlement to the dividend payment itself) on Tuesday 12th September 2023. The resolution is taken in accordance with BFF dividend distribution policy, and after a positive assessment on the possibility of distributing interim dividends during the year pursuant to Article 2433-bis of the Civil Code.

***

Significant events after the end 1H23 reporting period

Increase in Late Payment Interest rate

From 1-Jul-23, Eurozone Late Payment Interest (“LPI”) statutory rate increased by 1.5%, to 12.0% from previous 10.5%.

DBRS Morningstar Rating

As announced with the press release dated 19th July 2023, DBRS Morningstar (“DBRS”) has for the first time assigned its ratings to the Group, with Long-Term Deposits classified as Investment Grade at BBB (low) with stable outlook. This rating reflects BFF’s sound liquidity position and the improvement of its funding profile since the acquisition of DEPObank. The rating further strengthens the Banks’s operations in the Italian market of Securities Services and Banking Payments.

Board of Directors slate process

BFF Board of Directors started the process to present its own slate, in full alignment with best corporate governance market practice. The appointment of the new Board of Directors will take place at the Annual General Meeting in April 2024 approving the Financial Statements as of 31 December 2023, coinciding with the maturity of the term of office of the current Board of Directors. To allow maximum flexibility to the Board and the shareholders, the CEO Golden Parachute provision, triggered in the event of non-renewal of the office of CEO at the expiration of the term of office, has been removed. Therefore, no compensation will be paid to him in the event of actual non-renewal in the office. These changes in the contractual provisions were based on a settlement with the CEO, subject to all the Group Remuneration Policy provisions on variable remuneration .

***

Statement of the Financial Reporting Officer

The Financial Reporting Officer, Giuseppe Manno, declares, pursuant to paragraph 2 of article 154-bis of the Legislative Decree n° 58/1998 (“Testo Unico della Finanza”), that the accounting information contained in this press release corresponds to the document results, accounting books, and records of the Bank.

***

Earnings call

1H 2023 consolidated results will be presented today, 3rd August, at 15:00 CET (14:00 WET) during a conference call, that can be followed after registering at this link. The invitation is published in the Investors > Results > Financial results section of BFF Group’s website.

Consolidated Balance Sheet (Values in €)

Consolidated Income Statement (Values in €)

Consolidated capital adequacy

Asset quality