Comunicati Stampa - Italia - BFF Banking Group

Press Releases

The Board of Directors of BFF Bank S.p.A. today approved the consolidated financial statements for the first quarter 2022

- €38.1m Adjusted Net Profit, +37% YoY, with €13.4m of pre tax synergies in Corporate Center, steady growth in Securities Services and Payments, and recovery in Factoring & Lending. €31.3m Reported Net Profit

- Strong capital position: CET1 ratio at 16.7% and TCR at 23.2%, increased capital flexibility with €150m AT1 issued in Jan-22

- Excellent asset quality with annualized Cost of Risk at 1.1bps on loans

- Half-year dividend distribution after 1H22 results in Aug-22, €38.1m already accrued in 1Q22

- Well positioned in a raising interest rate environment

- No exposure to Ukrainian and Russian markets

- Signed an agreement for the acquisition of MC3 Informatica S.r.l., an IT consulting company based in Brescia, with closing subject to the expiry of the of 90-day period required for the prior notification to Bank of Italy.

Milan, 11thMay 2022 – Today the Board of Directors of BFF Bank S.p.A. (“BFF” or the “Bank”) approved the first quarter 2022 consolidated financial accounts, one year after the acquisition and merger by incorporation of DEPObank – Banca Depositaria Italiana S.p.A. (“DEPObank”) into BFF, with accounting and fiscal effect from 1st March 2021 .

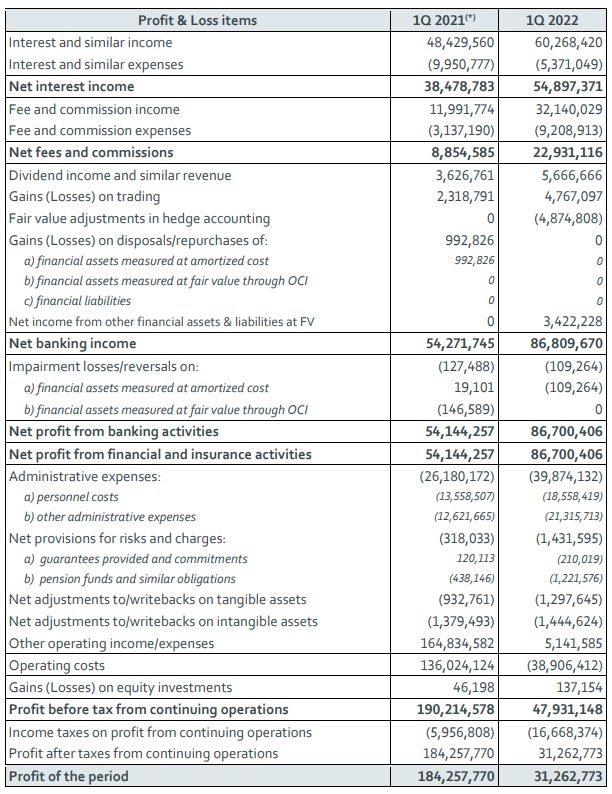

CONSOLIDATED PROFIT AND LOSS DATA

1Q22 Adjusted Net Revenues were €92.0m, of which €38.3m coming from Factoring, Lending & Credit Management, €14.6m from Securities Services, €14.9m from Payments, and €24.2m from Corporate Center (including synergies). Total Adjusted operating expenditures, including D&A, were €(36.8)m, and Adjusted LLPs and provisions for risks and charges were €(1.4)m .

The resulting Adjusted Profit before Tax was €53.8m and Adjusted Net Profit was €38.1m (+37% YoY), despite €(5.7)m of mark-to-market (M2M) impact related to the ex-DEPObank Held to Collect (“HTC”) bond portfolio, accounted in the Corporate Center business unit, while 1Q22 Reported Net Profit was €31.3m (for details see footnote n°2).

With regard to business units’ KPIs and adjusted Profit & Loss data, as of 31st March 2022, please refer to the “1Q 2022 Results” presentation published in the Investors > Results > Financial results section of BFF Group’s website. Please note that the Corporate Center comprises all the revenues and costs not directly allocated to the three core business units (Factoring, Lending & Credit Management, Securities Services and Payments), as well as the M2M accounting effect on ex-DEPObank HTC bond portfolio.

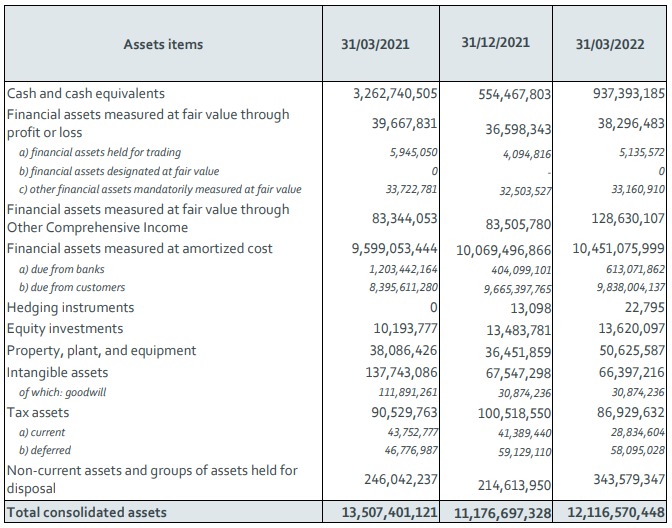

CONSOLIDATED BALANCE SHEET DATA

As of 31/03/2022, the consolidated Balance Sheet amounted to €12.1bn, up by €0.9bn compared to 31/12/2021 (+8% QoQ).

With respect to Total Assets, 1Q22 loan book was at €3,712m, almost at the same level of YE21 (at €3,745m as of 31/12/2021), with Italy up by 4%. It is important to notice that, due to a sesonality effect, the first quarter loan book is usually lower than the year end one. On a YoY comparison, 1Q22 loan book was up by 11%, with growth across all markets but Spain (still negatively impacted by high liquidity). Main increases in Total Assets are related to active Repos up by +0.2bn (+52% QoQ), to the HTC Portfolio up by +€0.1bn (+2.4% QoQ) and to the liquidity reported in Cash and Cash Balances up by €0.4bn, (+69% QoQ). At the end of March 22, the Government bond portfolio was classified entirely as HTC and amounted to €5.9bn vs. €5.8bn as of YE21 (+€0.1bn), out of which €2.9bn was fixed rate, with a duration of 28 months and a yield of 0.22%, and the remaining €3.0bn floating, with a duration of 37 months and a spread +0.62% based on Euribor 6M as of 31st March at (0.37)%.

The M2M after taxes (not recognized neither in the P&L nor in the balance sheet due to the HTC classification) is positive at €5.5m, with a reduction QoQ (€30.8m at 31/12/2021), due market volatility, especially at the end of 1Q22.

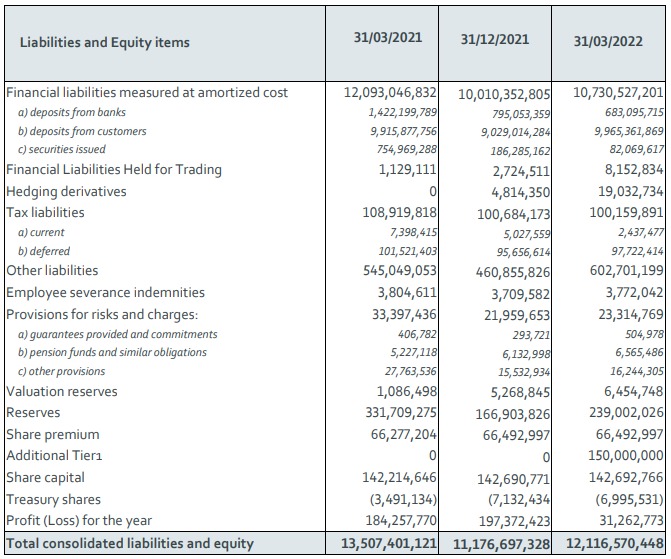

On Total Liabilities side, passive Repos were up by +€1.7bn (+148% QoQ), while deposits from Transaction Services decreased by €(0.84)bn, down (11)% QoQ, to maintain liquidity in ECB below the tiering level.

The main changes of BFF’s funding sources vs YE21 are the following:

- on-line retail deposits increased to €245m, (+6% vs. YE21), due to the campaign launched in Poland to benefit from the positive spread between funding cost, lagging behind the increase in WIBOR, and assets’ yield,

- Tier II Bond (€100m nominal value) was fully repaid on the call option date (2nd March), following the authorization received from Bank of Italy,

- a €150m perpetual NC 5 AT1 Bond was issued, with a fixed rate coupon of 5,875% per annum to be paid on a semi-annual basis, allowing for higher capital flexibility, large exposure limit and leverage ratio,

- BFF bonds outstanding marginally decreased to €81m, vs. €82m at YE21, after additional buy-backs during the 1Q22,

- refinancing operations related to Italian Government Portfolio increased at €2.8bn, (up by 1.7bn QoQ).

The Group maintained a strong liquidity position, with Liquidity Coverage Ratio (LCR) at 252.3% as of 31/03/2022. The Net Stable Funding Ratio (NSFR) and the leverage ratio, at the same date, were equal to 161.9% and to 4.7% respectively. Since 2Q21, the NSFR is positively impacted by the new regulation, which establishes more favorable weighting factors for the assets and liabilities related to factoring activities. The leverage ratio was positively impacted by the issuance of the AT1.

***

An illustrative analysis of the sensitivity to interest rates has been performed, considering an instantaneous parallel shift in interest base rate curves. For additional details on the please refer to page 12 of the presentation “1Q 2022 Results”.

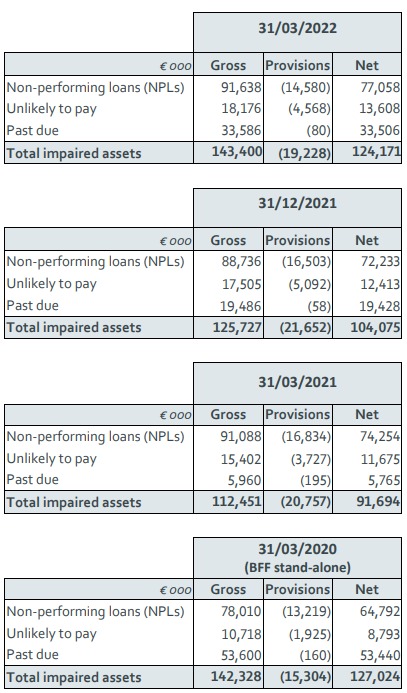

Asset quality

The Group continues to benefit from a very low exposures towards the private sector, with a negligible credit risk. Net non-performing loans (“NPLs”), excluding Italian Municipalities in conservatorship (“in dissesto”), were €7.4m, at 0.2% of net loans (2% including Italian Municipalities in conservatorship), with a 68% Coverage ratio. CET1 was not materially impacted by calendar provisioning.

The excellent asset quality is confirmed, with an annualized Cost of Risk of 1.1 basis points in 1Q22 (while it was slightly negative at YE21 and 1Q21 due to a release of provisions).

The increase in total net NPLs to €77.1m in 1Q22, from €72.2m at YE21 was driven by new exposure of Italian Municipalities in conservatorship (which increased to €69.7m in 1Q22 from €64.5m at YE21). It is important noticing that Italian Municipalities in conservatorship are classified as NPLs by regulation, despite BFF is legally entitled to receive 100% of the principal and late payment interests at the end of the conservatorship process.

At the end of 1Q22 net Past Due amounted to €33.6m, compared to €19.4m and €5.8m at the end of Dec-21 and 1Q21 respectively, due to some specific enforcements which negatively impact the Past Due, but help to maximize recovery.

Total Net impaired assets (non-performing, unlikely to pay and past due) were €124.2m as of 1Q22 (€104.1m at YE21 and €91.7m as of 1Q21), 82% of which were towards public sector. Net impaired assets net of “dissesti” were €54.5m at the end of 1Q22 (vs. €39.6m of BFF at YE21 and €23.8mln at 1Q21).

At the end of 1Q22 moratoria loans were €1.9m (net value).

Capital ratios

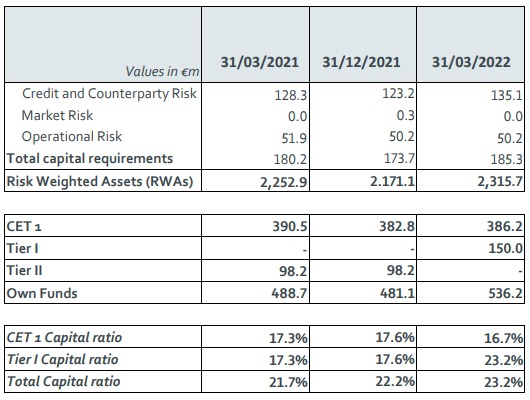

The Group maintains a strong capital position with a Common Equity Tier 1 (CET1) ratio of 16.7%, and a Total Capital ratio (TCR) of 23.2% (well above both the Bank’s TCR target of 15.0%), with €189m of capital in excess of 15.0% TCR target. The Total Capital and Tier 1 ratios benefited also from the issuance of the AT1.

Both ratios exclude €38.1m of accrued dividends. Including the adjusted net profit already accrued, CET1 ratio and TCR would be 18.0% and 24.5% respectively.

BFF did not to apply any of the ECB / EBA emergency measure or the European Commission’s banking package for COVID-19.

Risk-Weighted Assets (RWAs) calculation is based on the Basel Standard Model. 1Q22 RWAs were €2.3bn (vs. €2.2bn at YE21 and €2.3bn at 1Q21), with a density of 44%, vs. 45% at YE21 and 41% at 1Q21.

***

Significant events after the end of the 1Q 2022 reporting period

Dividend Payment 2021. Following the resolution of the Shareholders' Meeting of BFF held on 31st March 2022, the final amount of the gross dividend per share, equal to €0.6795, was paid starting from 21st April 2022. The gross dividend per share was calculated taking into account the number of BFF outstanding ordinary shares (185,315,280), and the treasury shares (970,366) held by the Bank.

Increase in interest rates in Poland. In Poland, the central bank's reference rate (WIBOR) increased from 0.10% at the end of 1H21, to 3.50% as of 31st March 2022, and to 5.25% at the end of the first week of May 2022. In this scenario BFF increased its funding in Zloty on the retail market in Poland by resetting the rates of the Lokata Facto to levels corresponding to negative spreads compared to the reference WIBOR.

Notice of Ordinary General Meeting of Shareholders. Today, following the press release published on 6th May 2022, the Board of Directors of BFF resolved to call an Ordinary shareholders' meeting on a single call, on 22nd June 2022 at 9:00 am, to proceed with the integration of the Board of Statutory Auditors and the appointment of its Chairman.

Signing of MC3.Today, following the resolution of the Board of Directors of BFF, it was signed an agreement for the acquisition of MC3 Informatica Srl (“Mc3”). MC3 is a company based in Brescia, which operates in the IT consulting sector with 7 employees and 4 external collaborators (www.mc3info.com ). BFF has been collaborating with MC3 for ten years, especially in the field of factoring systems: MC3, in fact, supported BFF in the initial implementation and subsequent evolution of the current core-factoring system of the Bank. The transaction is consistent with the growth path outlined by the Bank in its 2023 Business Plan, as it allows the vertical integration of all MC3’s development activities connected with the management and evolution of the information system into the Factoring & Lending business unit. Closing is subject to the expiry of the of 90-day period required for the prior notification of the acquisition to Bank of Italy.

***

Statement of the Financial Reporting Officer

The Financial Reporting Officer, Claudio Rosi, declares, pursuant to paragraph 2 of article 154-bis of the Legislative Decree n° 58/1998 (“Testo Unico della Finanza”), that the accounting information contained in this press release corresponds to the document results, accounting books, and records of the Bank.

***

Earnings call

The 1Q22 consolidated results will be presented today, 11th May 2022, at 2pm CET (1 pm WET) during a conference call, that can be followed after registering at this link. The invitation is published in the Investors > Results > Financial results section of BFF Group’s website.

Consolidated Balance Sheet (Values in €)

Consolidated Income Statement (Values in €)

(*) The Income Statement as of March 31, 2021 does not includes the balances of DEPObank of January and

February prior to the merger.

Consolidated capital adequacy

Asset quality